Choosing between FOB and CIF Incoterms is more than a cost calculation—it’s a critical decision about risk and control. With CIF, the buyer assumes all risk the moment goods are loaded onto the vessel, yet the seller maintains control over the carrier and insurance. This mismatch often creates hidden costs and logistical blind spots for importers.

This guide defines the precise risk boundaries for both FOB and CIF, explaining the modern ‘on board’ rule that dictates responsibility. We’ll show why the seller’s standard CIF policy provides only minimal insurance (Institute Cargo Clauses C) and how buyers can pay 10-20% more for a contract that gives them less control and inadequate protection against common shipping issues.

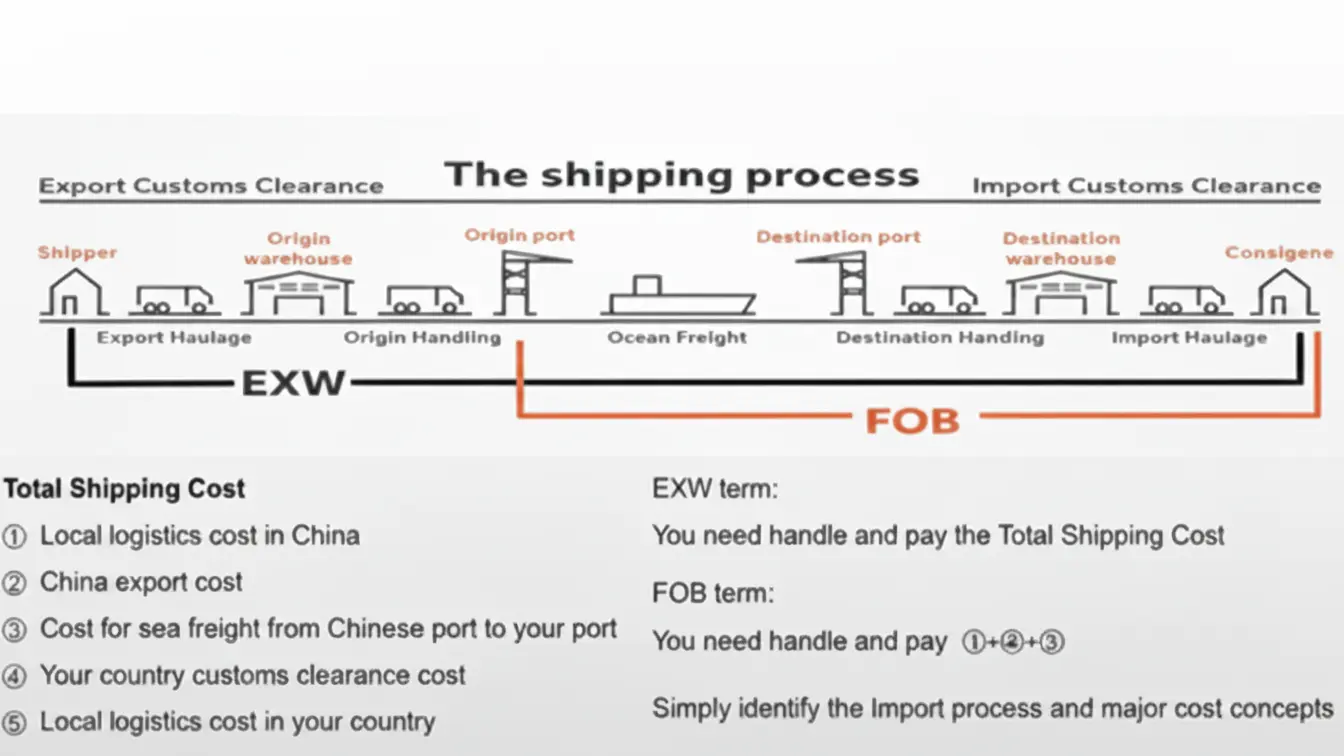

FOB (Free On Board): Definition and Buyer Responsibilities

Under FOB (Free On Board), the seller’s responsibility ends once goods are loaded onto the buyer’s nominated vessel at the specified port. At that moment, the buyer assumes all risks and costs, including ocean freight, insurance, and import clearance for the rest of the journey.

| Seller’s Responsibilities | Buyer’s Responsibilities |

|---|---|

|

|

Seller’s Duty: Getting Goods ‘On Board’

Under FOB terms, the seller’s primary responsibility is to deliver the goods and load them onto the vessel nominated by the buyer at the agreed-upon port of shipment. Risk officially transfers from seller to buyer as the goods are loaded on board the ship, a key point defined in the Incoterms 2020 rules. The seller is also required to handle and pay for all export clearance documentation and procedures in the country of origin. FOB terms are strictly for sea or inland waterway transport and should not be used for shipments moving by air, rail, or multiple transport modes.

Buyer’s Control: Managing Freight and Risk

The buyer nominates the ocean carrier, which gives them direct control over freight costs, transit times, and service levels. From the moment goods are on board, the buyer is responsible for all subsequent costs, including ocean freight, marine insurance, unloading charges, and import duties. Legal title and the risk of loss or damage pass to the buyer at the port of loading, an event typically confirmed by the issuance of an ‘on board’ bill of lading. The buyer also handles all import customs formalities and arranges for final delivery from the destination port to their warehouse.

CIF (Cost, Insurance, Freight): Hidden Risks for Buyers

Under CIF, the buyer assumes all risk for the goods once they are loaded onto the ship, yet the seller controls the shipping and provides only minimal insurance. This creates hidden risks related to inadequate coverage, lack of carrier control, and unexpected costs at the destination port.

| Risk Area | Seller’s Obligation | Buyer’s Hidden Exposure |

|---|---|---|

| Logistical Control | Chooses the carrier and manages the freight contract. | Assumes all risk for the main voyage but has no control over the carrier or routing. |

| Insurance Coverage | Provides minimum insurance (Institute Cargo Clauses C). | Coverage is not ‘all-risks’ and is often inadequate, leaving the buyer liable for uncovered damages. |

| Destination Costs | Pays for freight to the named destination port. | Responsible for all post-arrival charges: unloading, terminal fees, import duties, and inland transport. |

Risk Transfer vs. Logistical Control Mismatch

The fundamental problem with CIF lies in the disconnect between when risk transfers and who controls logistics. The buyer becomes responsible for the goods as soon as they are loaded onto the ship at the origin port. Yet, the seller retains full control over choosing the shipping line, the vessel’s route, and the freight contract. This arrangement puts the buyer in a vulnerable position, bearing all risk for loss or damage during the main sea voyage without any direct power to manage the carrier or the shipping process.

Inadequate Insurance and Hidden Destination Costs

CIF terms also introduce significant financial risks. The seller is only required to provide minimum insurance coverage (Institute Cargo Clauses C), which is not an ‘all-risks’ policy and leaves the buyer exposed to many common types of damage. The CIF price does not cover costs after the ship arrives. The buyer must pay for all destination charges, including terminal handling, unloading fees, import duties, and inland transportation. For containerized cargo, other Incoterms like CIP are better suited. Buyers often pay 10-20% more for a CIF price than for FOB, getting less control and only baseline insurance in return.

EXW (Ex Works): When to Use It (Consolidation Only)

Under the EXW Incoterm, the seller’s only job is to make goods available at their factory. It is best used by experienced buyers who want to consolidate shipments from multiple suppliers in the same country to save on freight, as the buyer handles all export clearance, loading, and transport.

How EXW Supports Shipment Consolidation

The main advantage of using the EXW Incoterm is for shipment consolidation. The seller’s responsibility ends once the goods are ready for pickup at their location, like a factory or warehouse. This arrangement gives a buyer the flexibility to collect orders from multiple suppliers in the same area. By combining these different orders into a single container at the point of origin, the buyer can substantially lower their total freight expenses.

Buyer Responsibilities and Practical Limitations

Under EXW, the buyer takes on nearly all responsibilities after the goods are made available. This includes loading the cargo, arranging every leg of transport, and managing all customs procedures for both export and import. The risk and cost transfer to the buyer at the seller’s door.

While effective for domestic trade, EXW presents significant challenges for international shipping. Buyers might need a legal presence in the seller’s country to handle export clearance. The term is also a poor fit for payments made by Letter of Credit and can complicate VAT reclaim due to a lack of formal export proof from the seller. A notable exception is a ‘Routed Export Transaction,’ where a foreign buyer appoints a freight forwarder to manage export logistics from the origin country on their behalf.

Partner with a Direct Manufacturer for Custom Commercial Umbrellas

DDP (Delivered Duty Paid): Is it Worth the Extra Cost?

DDP (Delivered Duty Paid) places maximum responsibility on the seller, who pays for all transport, insurance, and import duties to your door. It’s worth the cost for simplicity and predictable pricing, but experienced buyers often prefer other terms to control freight costs and avoid hidden markups on duties.

Seller’s Maximum Responsibility and Costs

Under DDP, the seller is responsible for 100% of transport risks, costs, export/import clearance, duties, and taxes until the goods are delivered to the buyer’s destination. This arrangement shifts the entire logistics and compliance burden from the buyer, creating a single ‘door-to-door’ price. The buyer’s obligations are minimal, typically limited to unloading the goods upon arrival and assisting with documentation if requested by the seller.

Cost vs. Control: Deciding if DDP is Right for You

DDP provides a clear, landed cost, which is ideal for buyers new to importing or those seeking budget certainty without managing logistics. Experienced importers often avoid DDP because sellers may add a markup to import duties and taxes they are unfamiliar with, increasing the total cost. While convenient, relying on the seller for import clearance exposes the shipment to potential delays if the seller lacks expertise in the destination country’s customs procedures.

Risk Transfer Points: The “Ship’s Rail” Rule

The “ship’s rail” was a rule from older Incoterms where risk transferred from seller to buyer once goods crossed an imaginary line at the ship’s side. This vague concept was replaced in Incoterms 2010 and 2020 with the clearer, physically verifiable rule where risk transfers when goods are placed ‘on board the vessel’.

The Historical ‘Imaginary Line’ for Risk Transfer

Under Incoterms 2000 and earlier versions, risk for FOB, CFR, and CIF shipments transferred at the moment goods passed “over the ship’s rail” at the loading port. This concept was widely criticized as an “imaginary line” because it did not reflect the physical handling of modern cargo. The rule’s ambiguity made it difficult to verify the exact transfer point in practice, often leading to liability disputes between sellers and buyers.

The Modern Rule: ‘On Board’ the Vessel

The International Chamber of Commerce (ICC) officially removed all references to the “ship’s rail” with the introduction of Incoterms 2010. Under the current rules, risk for FOB, CFR, and CIF transfers only when the goods are physically placed “on board” the vessel at the named port of shipment. This modern standard creates a clear, auditable event that aligns with official documentation like a ship’s loading logs, mate’s receipts, and the issuance of bills of lading.

Insurance Clauses: What Standard CIF Doesn’t Cover

Standard CIF insurance provides only minimum coverage via Institute Cargo Clauses (C). This policy covers major incidents like the ship sinking but excludes common risks like theft, breakage, contamination, war, or strikes. The buyer is responsible for insuring against these frequent issues, as the seller’s policy ends at the destination port.

Minimum Coverage: The Institute Cargo Clauses (C)

Under CIF Incoterms, the seller is only obligated to provide the most basic level of insurance, specified as Institute Cargo Clauses (C). This is a “defined risks” policy, which means it only covers a specific list of major events and disasters. It is fundamentally different from broader “all-risks” policies, such as Clauses (A), which cover a wider range of potential cargo damage.

The policy is required to cover at least 110% of the invoice value, which accounts for the cost of the goods, freight, and a 10% buffer for anticipated profit. Sellers often use this minimal clause because it satisfies their contractual obligation at the lowest possible cost. This practice effectively transfers the burden of insuring against more common, but less catastrophic, risks directly to the buyer.

Common Exclusions and Hidden Claim Requirements

The standard Clauses (C) policy explicitly excludes many of the most frequent shipping incidents. It does not cover losses from theft, contamination, or breakage. Separate clauses must be added at the buyer’s expense to protect against risks like war or strikes. The coverage is also strictly port-to-port, meaning the insurance contract terminates once the cargo is unloaded at the destination port, leaving inland transit uninsured.

Successfully filing a claim depends on precise documentation. The policy must be assignable, allowing the buyer to file a claim directly with the insurer without involving the seller. Critically, the cargo’s HS code classification must be accurate on all paperwork. A mismatch in HS codes is a common reason for claim rejection, especially as global tariff schedules continue to be updated.

Calculating Landed Cost: Duty, VAT, and Freight

Landed cost is the total expense to get a product from the factory to your warehouse. It includes the product price plus all freight, insurance, customs duties, and VAT. Calculating it correctly is essential for accurate pricing and margin analysis, as it reveals the true cost per unit.

The Core Formula for Landed Cost

The total landed cost is the sum of several components: the product cost, international freight (ocean or air), inland transport at both origin and destination, insurance, customs duty, and VAT or GST. This calculation also includes smaller service fees like customs brokerage, port handling, and documentation charges to arrive at a true door-to-door price. Your starting point for the calculation depends on the Incoterm used. For example, under FOB terms, you add freight and insurance costs, but under CIF terms, these are already included in the initial value.

A Step-by-Step Calculation Example

First, you must determine the customs value, which is often the CIF price of the shipment. If a shipment has a CIF value of $13,500 and the applicable tariff is 5%, the customs duty is $675. Next, you calculate the VAT on the combined total. Many authorities apply VAT to the sum of the CIF value and the duty. A 19% VAT on ($13,500 + $675) adds another $2,693.25. This brings the final landed cost at the port to $16,868.25, which is the total before you add fees for local delivery to your final warehouse destination.

Why Factories Prefer FOB Pricing

Factories prefer FOB pricing because it simplifies their role. They are only responsible for getting goods to the designated port and loaded onto the ship. This allows them to quote a clean product cost without worrying about unpredictable international shipping fees, insurance, or potential logistics markups, which become the buyer’s responsibility.

Simplified Costs and Reduced Risk

FOB pricing allows factories to quote a clear price for production without embedding unpredictable shipping expenses or markups. Once the goods are loaded onto the vessel, the responsibility and liability for ocean freight, insurance, and logistics shift entirely to the buyer. This transfer significantly reduces the factory’s administrative burden, freeing them from managing international carriers, complex customs procedures, and in-transit risks.

Empowering Buyers with Logistics Control

This arrangement also benefits buyers, particularly those with established logistics networks. FOB enables them to negotiate their own competitive freight rates directly with preferred carriers. It gives them direct control over their supply chain, including carrier selection for better real-time GPS tracking and ETA forecasts. This creates predictable, itemized landed costs—such as ocean freight and duties—without any hidden supplier margins on logistics.

Final Thoughts

Choosing between FOB and CIF comes down to a trade-off between control and convenience. FOB gives you direct control over your shipping, which often leads to better freight rates and more reliable transit times. While it requires more work, it gives you full visibility into your supply chain. CIF seems simpler because the seller arranges everything, but this convenience hides risks like minimal insurance coverage and a lack of control over the carrier.

The right Incoterm aligns with your business strategy. If you value cost management and supply chain control, FOB is almost always the better choice. If you prioritize simplicity and are willing to accept the associated risks and potentially higher costs, CIF or DDP might work. Understanding these risk boundaries helps you avoid unexpected fees and protect your cargo from the factory to your warehouse.

Frequently Asked Questions

What is the difference between FOB and CIF incoterms?

Under FOB (Free on Board), the seller’s responsibility ends once goods are loaded onto the vessel. From that point, the buyer arranges and pays for the main ocean freight and insurance. With CIF (Cost, Insurance, and Freight), the seller pays for ocean freight and minimum insurance, but the risk of loss transfers to the buyer as soon as the goods are loaded on the vessel.

Which incoterm is safest for first-time importers?

DDP (Delivered Duty Paid) is often considered the safest for new importers. The seller is responsible for all shipping, insurance, customs clearance, and import duties, delivering the goods directly to the buyer’s final location.

Does an FOB price include shipping to my country?

No. An FOB price covers the seller’s costs only up to the point of loading the goods onto the vessel at the port of origin. The buyer is responsible for paying for the main ocean freight, insurance, and all costs associated with importing and final delivery.

Who pays for insurance under CIF terms?

In a CIF contract, the seller is required to purchase and pay for marine insurance on behalf of the buyer. This cost is included in the CIF price. It is important to know this is typically only minimum coverage (Institute Cargo Clauses C), which may not cover all potential risks.